The FDNY Retirement Loan: Why There Is No Such Thing

When an FDNY member retires, the pension is calculated using several important numbers. These include final average salary (FAS), the 1/60th calculation, ITHP over 20, and sometimes other pension variables.

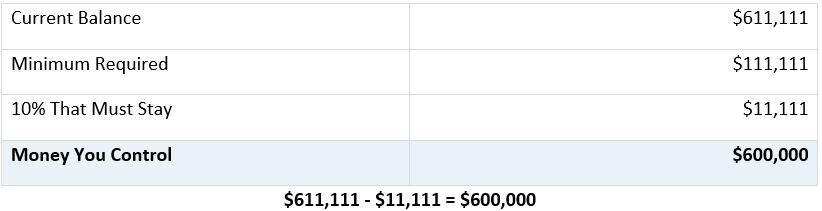

But there is one final number that often gets misunderstood: the “current balance” of the pension account. This is your pension account balance.

That current balance creates optionality, but it also requires a decision.

The key rule for everyone is simple: 10% of the Minimum Required amount must stay inside the pension.

Everything above that amount is Money You Control.

Here is a simple example:

In this example, the retiree has $600,000 of Money You Control. At retirement, you own that money.

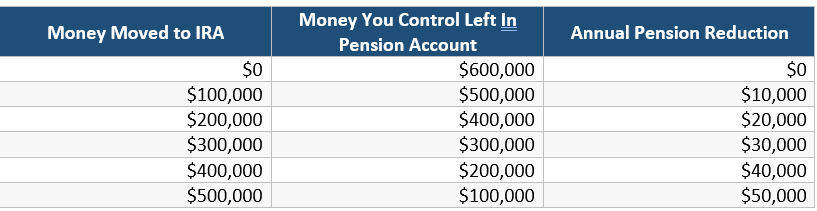

That money can be moved to a retirement plan, such as an IRA. The retiree can move all of it, some of it, or none of it.

But there is an important tradeoff: every dollar moved out reduces the pension. Every dollar left in increases the pension. This starts with the very first dollar removed.

The amount of pension change is driven by the Single Life Annuity Factor, or SLAF. The SLAF is the pension factor used to convert dollars in the pension account into annual pension income.

For illustration, assume a simple SLAF of 10. That means every $100,000 moved out of the pension account reduces the annual pension by $10,000 ($100,000 / 10).

Illustration: how the pension reduction moves dollar by dollar

This table is not a recommendation. It is simply showing how the math works.

In this example, the FDNY Retirement Estimate Report would show the last $100,000 removed as the “retirement loan”, equal to 90% of the Minimum Required amount. But as the table shows, the impact of removing that last $100,000 is exactly the same as removing the first $100,000, or any other $100,000 increment. The pension reduction is driven by the same SLAF calculation across the entire current balance.

The pension estimate report may highlight certain standard choices, but the underlying math works dollar by dollar.

The important point is that the math does not change.

There is no point where one dollar is treated differently than another dollar. There is no point where the economics suddenly become something else.

The retiree is simply deciding how much of the current balance to leave inside the pension and how much to move to a retirement account.

More money moved out means a lower pension. More money left in means a higher pension. However, money left inside the pension is no longer controlled by the retiree as a separate account balance; it is converted into a higher lifetime pension benefit. This decision is irrevocable.

Nothing we have analyzed implies that every retiree should make the same choice.

At Brave Eagle Wealth Management, we believe this decision should be made as part of the retiree’s complete retirement plan. The right answer depends on the retiree’s pension, investment portfolio, tax situation, and overall pension protection strategy.

For some retirees, it may make sense to leave more money inside the pension. For others, it may make sense to move more money to a retirement account. The important point is that the decision should be based on the numbers, not the label.

A real loan has principal that must be repaid. Here, there is no separate principal balance being repaid. There is only a pension adjustment based on how much money is moved out.

The FDNY retirement loan is not a loan.

There is no such thing as an FDNY retirement loan.

It is a choice about the Money You Control inside the pension account.