Research

Research Update: UFOA Market Portfolio Fee Now Reported at 0.29%

In October 2025, Brave Eagle Wealth Management published an independent review of the UFOA Market Portfolio fact sheet that identified two discrepancies: an asset-allocation misstatement (93.96% U.S. stock reported despite a 40.53% position in a U.S. debt index fund) and an expense ratio (fee) reported at 0.15% gross and net, versus our independently calculated weighted-average cost of approximately 0.30%.

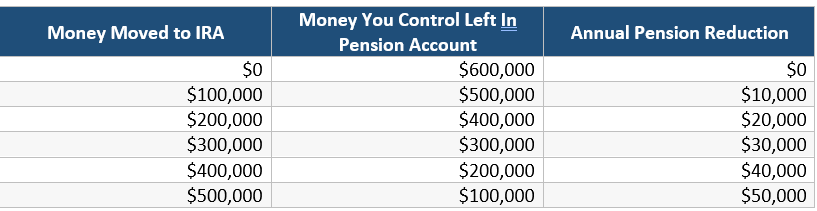

The FDNY Retirement Loan: Why There Is No Such Thing

When an FDNY member retires, the pension is calculated using several important numbers. These include final average salary (FAS), the 1/60th calculation, ITHP over 20, and sometimes other pension variables.

But there is one final number that often gets misunderstood: the “current balance” of the pension account.

How to Evaluate a Financial Advisor

Most FDNY retirees meet financial advisors through referrals, recommendations, or lists. That is a starting point — not the final decision. The real question: Does this advisor understand your situation and know how to put it all together?

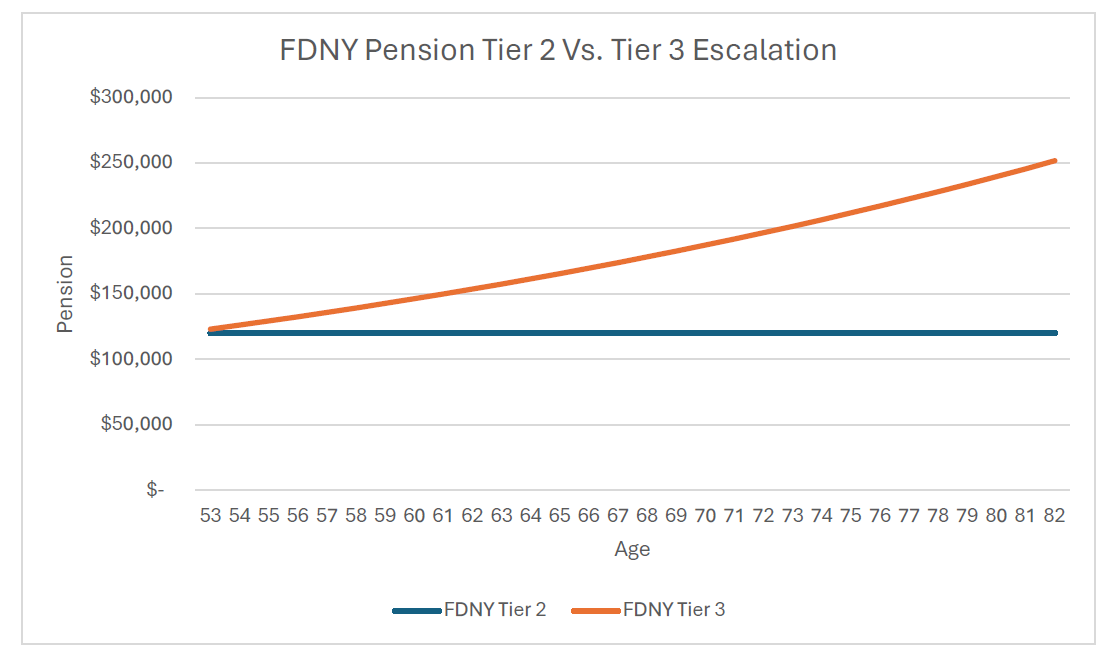

Tier 3 Pension Reform: A Capital-Markets Ranking of What Actually Matters

Across the prior three pieces, we evaluated the FDNY Tier 3 pension using the same framework capital markets apply to long-duration income streams: time, cash flow, and asset value.

FDNY Tier 3 Social Security Offset: The Structural Constraint

In the first piece, we quantified the Tier 3 pension change across three dimensions: time, cash flow, and asset value. That analysis focused on the floor of the pension — what a Tier 3 member is guaranteed at 20 years.

In the second piece, we examined the ceiling — escalation — how it is earned, why it matters economically, and what it is worth in present-value terms.

This final piece addresses the structural constraint on Tier 3 outcomes: the Social Security offset.

FDNY Tier 3 Escalation: Understanding the Real Ceiling

In the first piece, we quantified the Tier 3 pension change across three dimensions: time, cash flow, and asset value. That analysis focused on the floor of the pension — what a Tier 3 member is guaranteed at 20 years.

This piece addresses the ceiling of the Tier 3 pension.

Specifically, how escalation works, what is required to earn it, and how to think about its economic value using the same capital-markets lens.

To keep the analysis consistent, we continue to examine outcomes through the lens of a 52-year-old Tier 3 retiree, recognizing that individual results will vary.

The Tier 3 FDNY Pension Win: Quantifying the Time, Cash Flow, and Asset Value Impact

A capital-markets framework for understanding the most meaningful Tier 3 pension change in over a decade.

On December 19th, 2025, Governor Kathy Hochul signed SB4727 into law marking the most meaningful change to the FDNY Tier 3 pension system in over a decade. Stripped of politics and headlines, this legislation represents a structural improvement that can be quantified across three dimensions every Tier 3 member should understand:

NYS Audit Notices: What FDNY Retirees Need to Know

Over the past several weeks, there has been a noticeable increase in New York State audit notices issued to retirees regarding distributions from the Empower–Uniformed Fire Officers Association (UFOA) Annuity Plan. This development has understandably caused confusion and concern among retirees. While multiple factors may be contributing to this activity, two primary developments appear to explain the current increase in audit notices.

How to Read a Fact Sheet (FDNY Retiree Guide)

Fact sheets are short summaries of the investment options available in your retirement plan. They describe what a fund owns, its mix of stocks and bonds, and the expenses that come out of the investment option. Understanding Fact Sheets doesn’t require a finance degree—just knowing where to look.

Is It Worth Paying Empower’s Advisors in the UFOA Plan

Every firefighter knows the rule: before the tour starts, you check your gear and the rig and make sure everything is working the way it should. At Brave Eagle Wealth Management, we applied that same mindset to a portfolio built by an Empower advisor inside the UFOA Annuity Plan. Our analysis found that the portfolio—constructed from nearly every fund available in the plan—was redundant, costly, and confusing. It mixed multiple “one-stop” model portfolios that were never meant to be owned together and disclosed fees that appear inconsistent with the calculated costs of one of the plan’s one-stop model portfolios.

Is Private Equity Coming to Your Retirement Plans

Private equity and other private assets are making a push to be included in retirement plans alongside public securities investments. Empower, one of the largest retirement plan providers, recently announced that it will offer private investments inside of some retirement plans. Are private assets a good fit for retired FDNY?

Webinar: Roth IRA Conversions

Brave Eagle Wealth Management will be hosting an education webinar on Roth IRA conversions on July 22, 2025 at 1:00 pm.

Robert Ruggirello on Bloomberg TV

Robert Ruggirello was interviewed on Bloomberg TV. Robert discussed Nividia and other market topics.

Video-FDNY NYPD Final Average Salary

Brave Eagle Wealth has posted a video to the website. The FDNY-NYPD final average salary video is an educational video that active members might find helpful.

The 10-Year Certain Beneficiary Option: A Misunderstood Gem for FDNY Retirees

When FDNY retirees receive their pension finalization letter, the 10-Year Certain option is listed as one of the seven beneficiary options available. Yet, surprisingly, it remains untouched. This article explores the 10-Year Certain Option, its unique features, and how it can address the needs of FDNY retirees seeking a balance between cost and security.

The Importance of Isolating Rolled Over Pension Money

At retirement, some FDNY & NYPD Tier 2 members elect to rollover pension money (excess/overage, VSF DROP, etc.) into an IRA. At Brave Eagle Wealth Management we isolate the client’s pension rollover money in its own IRA, no other retirement plan money (NYC Deferred Compensation Plan 457, 401k, etc.) is rolled into the pension money IRA.

One Billion Dollars of Hidden Losses in NYC DCP’s Stable Income Fund

The Stable Income Fund is a crowd favorite across NYC Deferred Compensation Plan account types. In aggregate, 29.5% of total plan assets were invested in the Stable Fund, or $7.7B (Billion) of $26.2B, at year end 2022. In stark contrast, the Bond Index Fund only holds about 4.4% of plan assets even though this AA rated Bond Fund was offering the highest prospective returns in over a decade.

Roth Conversions and Federal Tax Brackets

A Roth conversion is when a taxpayer decides to move (convert) pre-tax retirement funds (IRA, 457, 401k, etc.) to a Roth IRA. A Roth conversion must take place during a tax year and once it is complete it cannot be undone. The conversion results in taxes being owed, in most cases. There are no income limits to do a Roth conversion and there are no limits on the amount that can be converted.

The Superannuated – A Ladder Strategy to Protect the Pension

FDNY retirees generally can choose between two tools to protect (hedge) the value of their pensions:

1. Pension Beneficiary Option

2. Term Life Insurance

The beneficiary option is available to all retirees. The cost depends on the age of the pensioner and the age of the beneficiary. Life insurance is available to those that are healthy enough to qualify for it.

Terminal Leave Lump Sum Tax Deferral Failures

Some FD retirees receive their terminal leave lump sum check without any of the funds being tax deferred even though they requested a certain tax deferral percentage before they retired. Why does this happen?